By expanding a pilot program for securitizing credit assets, could China's own subprime mortgage market be at risk?

The United States is home to a mature system of financial derivatives in which loans are packaged into securities and unleashed onto the market. These days, the practice is gaining momentum in China.

|

Lots of money: A clerk counts banknotes at a rural commercial bank in Ganyu county, Jiangsu province.[Photo / bjreview.com]

|

At the State Council executive meeting hosted by Premier Li Keqiang on August 28, a decision was made to further expand the pilot program for securitizing credit assets, while strictly controlling risks. A major push factor behind the campaign may be the liquidity crunch in China's banking sector at the end of June.

Lu Zhengwei, chief economist of Industrial Bank Co Ltd, said the popularization of credit asset securitization will motivate China's financial industry to liquidize remnant assets and better distribute its financial resources, all the while shoring up the real economy. Besides, using new capital properly and revitalizing existing assets make up the core of Premier Li's belief that the financial industry must be better used to support the real economy.

Start up

Credit asset securitization, though playing an important role in the developed world, is still in its infancy in China.

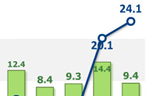

China started allowing credit asset securitization on an experimental basis in March 2005. A total of 11 domestic financial institutions issued asset-backed securities products worth 66.78 billion yuan ($10.91 billion) between 2005 and 2008, according to the People's Bank of China, the central bank.

Affected by the 2008 US subprime mortgage crisis and the global financial crisis, the pilot program struck a reef in 2009. It was not resumed until 2011, when six financial institutions issued ABS products worth 22.85 billion yuan ($3.74 billion).

Thanks to the pilot program that has lasted for eight years, a basic system of credit asset securitization has been established, with the issuance and trading of ABS products running smoothly and the initiators and investors becoming increasingly diversified, said the PBC.

However, compared with the United States, China's credit asset securitization is still in its preliminary stages. Statistics from some American financial institutions show that in the wake of the 2008 subprime crisis, the value of ABS products issued in the United States slumped from its peak of $2.9 trillion in 2006 to $1.5 trillion before the market began to recover gradually. The value of ABS products issued in 2012 reached $2.2 billion, up 26.9 percent year on year, accounting for 32.3 percent of bonds issued during the same period. The value of all existing ABS products stood at $9.9 trillion in 2012, making up 25.8 percent of existing bonds.

In stark contrast, at the end of March 2013, the value of existing ABS products in China was a mere 27.8 billion yuan ($4.54 billion), while the value of deposited bonds was 26 trillion yuan ($4.25 trillion). Yuan-denominated loans reached 66 trillion yuan ($10.78 trillion).

Significance

According to the PBC, China's financial macro-controls are under great pressure, and monetary loans are increasing rapidly. The expansion of credit asset securitization is beneficial in four respects.

It will be conducive to restructuring credit assets, encouraging reforms in key sectors like railway and shipbuilding, and intensifying credit support to projects like government-subsidized housing.

Commercial banks will distribute their core capital in a more efficient way, and the capital market can better finance the real economy.

It will also push commercial banks to shift from an expansion-driven operation model, reduce financing costs and boost intermediate business income.

Highlights of AOPA-China Flt-In air show

Highlights of AOPA-China Flt-In air show

Car Free Day to fight air pollution

Car Free Day to fight air pollution

Liaoning carrier completes its furthest sea trial

Liaoning carrier completes its furthest sea trial

798 Art Festival kicks off in Beijing

798 Art Festival kicks off in Beijing

Intl comic festival 'Comicopolis' held in Buenos Aires

Intl comic festival 'Comicopolis' held in Buenos Aires

Highlights of CIAPE 2013

Highlights of CIAPE 2013

2013 China International Auto Parts Expo kicks off in Beijing

2013 China International Auto Parts Expo kicks off in Beijing

Tesla, electric, hybrid cars at Frankfurt 2013 Motor Show

Tesla, electric, hybrid cars at Frankfurt 2013 Motor Show

Copyright 1995 - . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()